Missing year-end compliance deadlines in India introduces severe financial risks, including ₹100/day ROC late fees, deactivation of Director Identification Numbers, and tax disallowances under Section 43B(h). To close a financial year (April 1 to March 31) successfully, founders must coordinate GST, Income Tax, MCA, and Labour filings. This guide details key deadlines, tax audits, GSTR-9 reconciliations, and penalty schedules for FY26-27.

In India, year-end compliance refers to the mandatory statutory filings a business must execute to close the accounts and registers for the Financial Year (April 1 to March 31). It spans four key pillars: Income Tax (ITR & Tax Audits), GST (GSTR-9 annual returns), corporate governance (ROC filings under the MCA), and Labour Laws (PF, ESI, and bonus payouts). While the operational year closes in March, the regulatory deadlines cascade throughout the following months, extending up to December 31.

In my experience advising scaling startups and SMEs, the biggest risk is the last-minute scramble. Fragmented accounting systems and poor communication between bookkeepers and statutory auditors lead to filing delays and high interest expenses.

At EaseUp, we build proactive closing calendars to ensure clean audit trails. You can explore how we manage this process on our accounting and compliance page.

To prevent compliance leakages, print and track this master filing schedule for the financial year closing:

Compliance Category | Statutory Form / Section | Filing Frequency | FY26-27 Target Deadline | Late Fee & Penalty Schedule |

Goods & Services Tax | GSTR-1 (Outward Supplies) | Monthly | 11th of every month | ₹50 per day (₹20 for NIL return) |

Goods & Services Tax | GSTR-3B (Tax Payment) | Monthly | 20th of every month | ₹50 per day + 18% p.a. interest on cash tax |

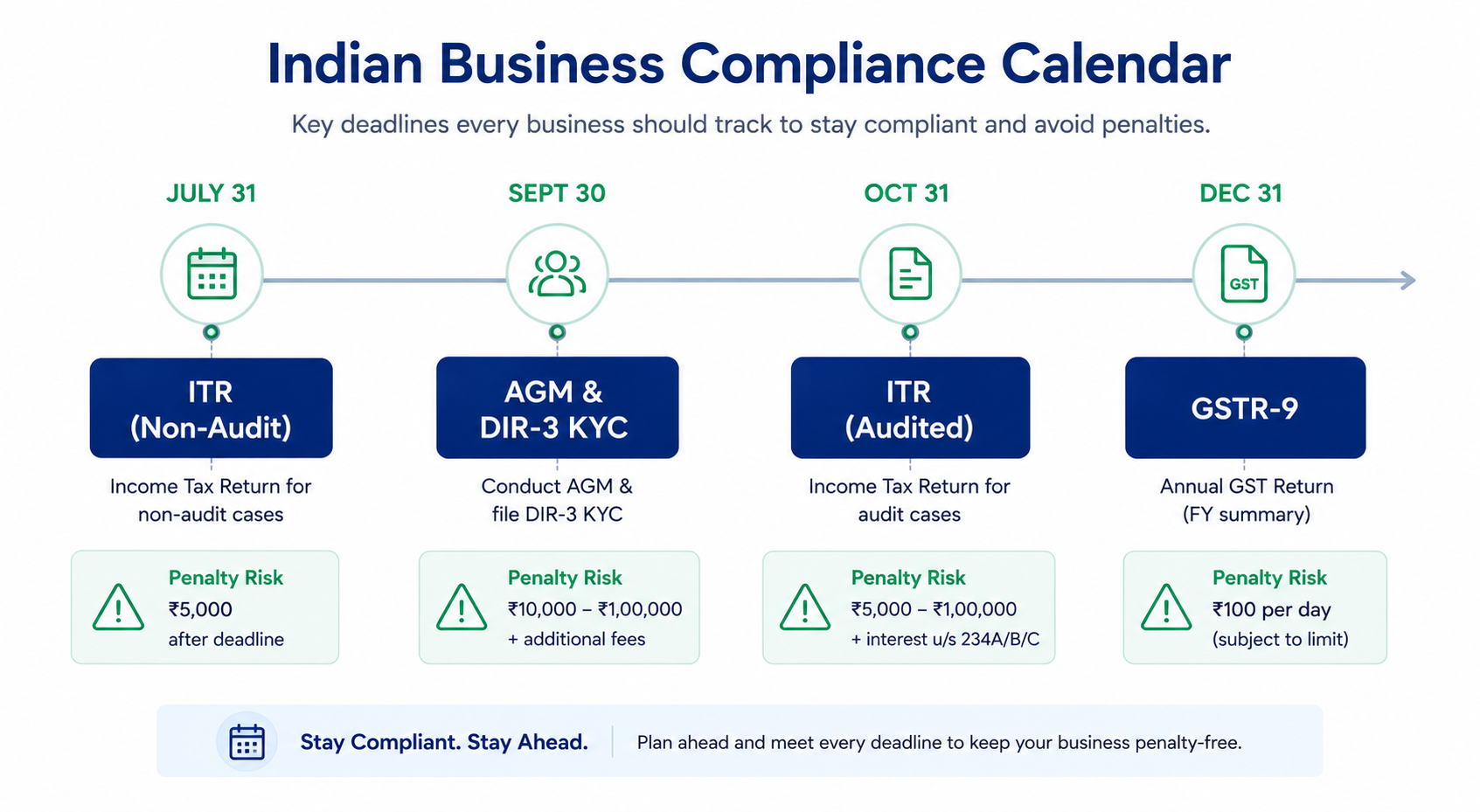

GST Annual Return | GSTR-9 / GSTR-9C (Reconciliation) | Annual | December 31, 2027 | ₹200 per day (capped at 0.25% of state turnover) |

Income Tax Return | ITR Filing (Tax Audit Cases) | Annual | October 31, 2027 | ₹5,000 late fee (Section 234F) + 1% monthly interest |

MCA / ROC Filing | AOC-4 (Financial Statements) | Annual | 30 days from AGM date | ₹100 per day per form (compounding daily) |

MCA / ROC Filing | MGT-7 (Annual Return) | Annual | 60 days from AGM date | ₹100 per day per form (compounding daily) |

Director KYC | DIR-3 KYC | Annual | September 30, 2027 | ₹5,000 penalty + deactivation of DIN |

Tax Deducted at Source | Form 26Q / 24Q (Quarterly TDS) | Quarterly | 31st of following month | ₹200 per day (Section 234E) |

Labour Compliance | PF & ESI Remittance | Monthly | 15th of every month | 12% - 25% p.a. damages + disallowance of expense |

GST year-end work should start with a simple 3-way match: compare your purchase register, GSTR-2B, and GSTR-3B. This helps you catch missing input tax credit, vendor mismatches, and filing errors before they lead to notices.

ITC Reconciliations: Identify vendors who have not uploaded invoices. Unmatched credits cannot be claimed, leading to direct cash losses.

Section 17(5) Reversals: Identify and reverse ineligible input tax credits (e.g., credit on motor vehicles, employee food/beverage, and personal expenditures).

GSTR-9 & 9C Limits: Filing GSTR-9 is mandatory if your turnover crosses ₹2 Crore. If turnover crosses ₹5 Crore, you must file GSTR-9C, which reconciles audited books with your GST declarations. To ensure complete compliance, check out our GST filing services.

Under the Income Tax Department guidelines, accurate reporting is critical to avoid scrutiny notices. Key areas of focus include:

A formal tax audit is mandatory if your business turnover exceeds ₹1 Crore (if cash transactions exceed 5% of total business volume) or ₹10 Crore (if digital transactions are 95%+ of total business volume).

100% of your estimated tax liability must be settled in quarterly installments by March 15. Shortfalls trigger interest penalties of 1% monthly under Sections 234B and 234C.

Ensure all TDS credits deducted by your clients are updated in your Form 26AS and Annual Information Statement (AIS) before filing your returns. Any discrepancy will lead to automated tax notices.

If you want to evaluate your company's tax position and prevent year-end tax penalties, book a free consultation with our CAs today.

Private Limited companies must comply with corporate governance rules managed by the Ministry of Corporate Affairs:

Board Meetings: Section 173 mandates a minimum of 4 board meetings in a calendar year, with a maximum interval of 120 days between consecutive sessions.

Annual General Meeting (AGM): Under Section 96, every company must hold its AGM by September 30 to adopt audited financials.

Filing Timelines: AOC-4 must be filed within 30 days of the AGM, and MGT-7 within 60 days. Missing these deadlines incurs a flat penalty of ₹100 per day per form.

Labour compliance carries heavy tax and legal implications if managed poorly:

Employees' Provident Fund (PF): Contributions must be deposited with the EPFO by the 15th of the next month. If payments are delayed, the employer's contribution is permanently disallowed as a business expense under Section 36(1)(va) of the Income Tax Act.

Form 16 Issuance: Employers must compile salary TDS and issue Form 16 to employees by June 15.

Bonus Provisions: Ensure statutory bonuses under the Payment of Bonus Act are provisioned in your books by March 31.

Indian SMEs must pay close attention to Section 43B(h) of the Income Tax Act, which went into effect recently:

Section 43B(h) Mandate: Payments to registered Micro and Small enterprises must be cleared within 15 days (if no written agreement exists) or 45 days (if a written agreement exists).

Tax Penalty: Any outstanding payment beyond these timelines as of March 31 will be disallowed as an expense. It will be added back to your taxable income, inflating your tax liability. The expense can only be claimed in the year you actually clear the dues.

Form MSME-1: Companies must file this half-yearly return to report outstanding MSME dues exceeding 45 days.

Ensure your compliance calendar is tailored to your business entity:

LLP Compliance: LLPs must file Form 11 (Annual Return) by May 30 and Form 8 (Statement of Accounts) by October 30.

FDI Companies (FEMA): Firms with foreign direct investment must file the annual FLA (Foreign Liabilities and Assets) return with the Reserve Bank of India by July 15.

Trusts & Section 8 NGO: Tax audit reports must be filed in Form 10B/10BB to claim tax exemptions.

Non-compliance carries heavy financial penalties:

GSTR-9 Delay: ₹200 per day, accumulating up to 0.25% of turnover.

DIR-3 KYC Delay: ₹5,000 late fee per director, and the DIN is deactivated, halting all MCA filings.

AOC-4 / MGT-7 Delay: ₹100 per day per form, with compounding penalties for directors.

TDS Return Delay: ₹200 per day under Section 234E, up to the total TDS amount deducted.

If you are looking to scale your finance stack, upgrading to a systemized partner prevents these costly leakages. Read about our virtual CFO services to see how strategic finance keeps your company compliance-secure.

Compile these files in a secure cloud directory before starting your audit:

Bank Statements: Complete logs for all accounts from April 1 to March 31.

Trial Balance & General Ledgers: Extracted from your accounting books.

GST filings archive: Consolidated GSTR-1 and GSTR-3B filings.

TDS Challans & Form 26AS: To reconcile tax credits.

Fixed Asset Register (FAR): Detailing additions and depreciation under Section 32.

Payroll Registers: Including employee salary details, PF, and ESI receipts.

Lease & Vendor Agreements: Enforcing statutory contracts.

Board Minutes Book: Documenting corporate resolutions.

ESOP Register: Detailing grants, vests, and exercises.

Related Party Transactions (RPT) Register: Reconciling transactions with directors.

Cap Table & Share Allotments: Reconciling equity.

FEMA / RBI filings: Reconciling foreign investments (Form FC-GPR/FLA).

Don't let year-end compliance stress you out. Let our team of chartered accountants handle all your statutory filings seamlessly.

Prioritize Section 43B(h): Review all supplier agreements and clear MSME vendor payments before March 31 to prevent tax disallowances.

Run 3-Way GST Matches: Reconcile GSTR-2B monthly to catch missing vendor invoices and secure your input credits.

File DIR-3 KYC Early: Avoid DIN blocks by completing director verification before September 30.

Consolidate Documents: Keep all 12 key financial folders updated in a cloud system to ensure a fast, hassle-free audit.

Missing the December 31 deadline for GSTR-9 attracts a late fee of ₹200 per day (₹100 CGST + ₹100 SGST), capped at 0.25% of your turnover in the state.

Yes, you can file a belated or revised return under Section 139(4) or 139(5) until December 31 of the assessment year, but it attracts a ₹5,000 penalty under Section 234F.

Yes, every individual holding a DIN as of March 31 must file DIR-3 KYC by September 30, regardless of whether the company is active or inactive.

Dormant companies must file Form MSC-3 (Return of Dormant Company) instead of AOC-4, to retain their dormant status under the Companies Act.

No, the Section 43B(h) disallowance for delayed MSME payments currently only applies to payments made to micro and small enterprises operating as manufacturers or service providers, not retail or wholesale traders.

Your trusted partner for all your Financial needs.

Finance Management

Strategic Services